The state of Ohio’s Brownfield Remediation Program incentive (BRP) was recently enacted by the Ohio General Assembly as part of budget sub-bill Sub. House Bill 33.

The BRP is to be funded with $350 million, split among two fiscal years.

Ohio is also funding another demolition incentive with a $150 million appropriation, for a total of $500 million in potentially-revitalizing investments.

Current language in the budget bill provides that $1 million in BRP funding is to be set aside for each county per year, with $87 million available on a first come, first serve basis statewide.

For counties with populations less than 100,000, the revised program requires that County Commissioners submit a recommended lead applicant to the Ohio Department of Development for approval.

For counties with populations greater than 100,000, county land reutilization corporations, or land banks, are designated as lead applicants, if the county has a land bank.

If such counties have no land bank, then County Commissioners must submit a recommended lead applicant to the Ohio Department of Development for approval. The BRP functions as a reimbursement grant.

A recent EPA commissioned study found that every $1 of EPA brownfields funds spent on assessment and cleanup activities leveraged an additional $19.78. The study also found that brownfields, due to their central location and connections to existing infrastructure, are often “location-efficient.”

This characteristic enables brownfield redevelopment to support job and housing growth.

Moreover, redeveloping brownfields contributes to a reduction in impervious surface expansion, which has positive implications for water and air quality.

Additionally, residential property values within 1.29 miles of former brownfields experienced increases ranging from 5% to 15%.

BROWNFIELD REDEVELOPMENT BENEFITS

- Increased potential for positive network effects;

- Job creation and economic development;

- Removal of blight;

- Reduced legacy cost burdens;

- Increased neighborhood appeal;

- Increased property value;

- Increased health outcomes;

- Enhanced sustainability outcomes;

- Creation of community or private development site; and

- Potential reductions in crime and poverty.

BROWNFIELD TAX INCENTIVES GENERALLY

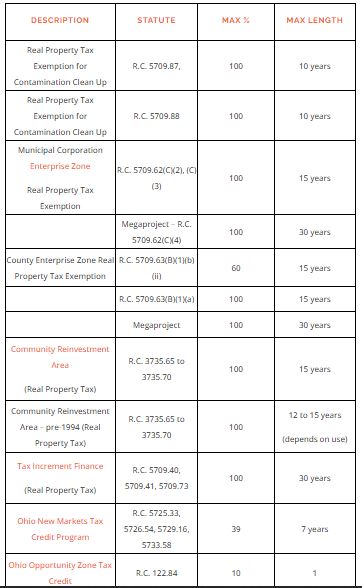

Other Ohio brownfield incentives not necessarily associated with environmental contamination are shown in this table.

Brownfield tax incentives provide substantial opportunity for the assessment, remediation and redevelopment projects of abandoned land, vacant land, and blighted areas.

Specifically, the brownfield tax incentives aim to encourage cleanup and redevelopment of brownfields by reducing the cost of eligible cleanup expenses.

Generally, a brownfield site is defined as a property where expansion, redevelopment or reuse is complicated by known or potential releases of hazardous substances, pollutants, contaminants.

The United States Environmental Protection Agency (EPA), which has substantial resources devoted to brownfields programs, has estimated that there are an estimated 450,000 to 1 million brownfields in the United States.

The Ohio Environmental Protection Agency’s (OEPA) database of voluntary listings has 369 sites in its inventory, but the Greater Ohio Policy Center has previously estimated that Ohio has closer to 9,000 brownfields.

Both the EPA and OEPA have numerous programs to fund brownfield assessment, remediation and redevelopment activities.

EPA provides funding for brownfields assessment, cleanup, revolving loans, environmental job training, technical assistance, training, and research through its Brownfields Program. OEPA currently administers 16 financial programs.

FEDERAL BROWNFIELDS TAX INCENTIVE PROGRAMS

At the Federal level, there are several brownfield tax incentives. The brownfields expensing tax incentive reduces taxable income by the cost of eligible cleanup expenses in the year the expenses are incurred.

There are three qualification requirements:

- The property is owned by the taxpayer incurring the eligible cleanup expenses, and used in a trade or business for the production of income;

- Hazardous substances or petroleum contamination must be present or potentially on the property; and

- Taxpayers must obtain a statement from a designated state agency that confirms the site is a brownfield site eligible for tax incentives. Participation in the state’s voluntary cleanup program satisfies this requirement.

According to EPA published guidance, eligible costs must be associated with: “Activities that control the release or disposal of a hazardous substance or petroleum contamination, or activities that abate the threat of a release or disposal of a hazardous substance or petroleum contamination.”

Other Federal brownfield incentives not necessarily associated with environmental contamination are New Markets Tax Credits which target distressed communities, Low Income Housing Tax Credits, Historic Preservation Tax Incentives, and energy efficiency and renewable energy credits, which have been recently enhanced through the Inflation Reduction Act.

UNLOCKING THE POTENTIAL OF BROWNFIELD TAX INCENTIVES FOR REDEVELOPMENT

Ample opportunity exists to take advantage of brownfield tax incentives to reactivate blighted, neglected, or underdeveloped sites, but lack of awareness or inherent complexities prevent brownfield incentives from being used more often.

There are numerous resources and advisors available to assist in planning for brownfield redevelopment and the utilization of incentives.

Ultimately, brownfield tax incentives provide an opportunity to garner projects that have a positive economic impact on blighted or abandoned areas.

Photo of Columbus, Ohio is by David Mark from Pixabay.

This article by KJK Economic Development & Incentives attorneys Richard A. Morehouse and Hannah R. Albion originally appeared on the website of Kohrman Jackson & Krantz LLP (KJK). Reprinted here (with minor edits) by permission.